Main Paper

Agentic Finance: Will AI use Crypto or Visa as Rails by Donovan (ex-crypto reporter), Darren (Tensorplex) 24 March 2026

Summary

AI agents need to pay each other. The internet's payment layer wasn't built for machines making thousands of micropayments per hour. A new stack is forming — from settlement chains to identity registries to reputation systems — to power autonomous machine commerce. The question isn't whether it happens. It's which layers capture the value.

Why This Is Important

The payment protocol works. The problem is everything around it — too few useful endpoints, no way for agents to find them, and no way to verify which ones are trustworthy. The investment opportunity isn't in payments. It's in the infrastructure layers that are still missing.

Current Protocols

(i) x402 protocol (Coinbase, May 2025) embeds stablecoin payments directly into HTTP requests using the 402 Payment Required status code (a http protocol code). (ii) Machine Payments Protocol (MPP), an open standard, internet-native way for agents and services to coordinate payments through stablecoins and fiat. It is co-authored by Tempo and Stripe. Tempo is a payment focused blockchain incubated by both Paradigm and Stripe. Stripe users can also accept payments over MPP in a few lines of code using the PaymentIntents API. (iii) Universal Commerce Protocol (UCP) - Developed by Google in collaboration with Shopify, Etsy, Target and Walmart to support the full shopping experience by acting as the standard language for AI agents to understand product listings, prices and checkout processes across multiple platforms.

Mismatch Against Reality

Visa, Mastercard, and Stripe are preparing for AI agents to transact autonomously, with Gartner estimating "machine customers" could influence $30 trillion in annual purchases by 2030. Yet on-chain data suggests reality lags the narrative: excluding bots and speculative token minting, organic x402 volume is 95% below peak.

Missing Pieces

Agentic commerce infrastructure is still early. (i) Discovery: Service discovery is fragmented across competing registries like Clawhub, Claude Marketplace, Tempo, and Coinbase Bazaar, each with its own standards. This creates a "fragmentation tax" for developers and agents, who must integrate across multiple systems. Metadata also needs to be structured and machine-queryable, since errors could cause agents to pay for services they never receive. (ii) Identity: Agents need a reliable way to prove who they are and who authorized them. ERC-8004 and Visa's Trusted Agent Protocol are competing to become the dominant identity layer, with strong winner-take-most dynamics. The WEF has also called for a "Know Your Agent" framework alongside KYC. (iii) Security: Weak identity and discovery create major fraud risks. A malicious actor could impersonate a trusted provider, list fake services, and drain agent wallets at machine speed. Unlike traditional fraud, agentic scams can spread instantly and hit many victims before humans notice.

Example

A vibe coder can build a financial data API in 4 hours. She adds x402, and charge $0.001 per request in USDC on Base — no website, legal entity, Stripe account, or merchant onboarding needed. Another agent can call it 40,000 times and generate $40 in revenue. But if that same agent wants satellite imagery of Singapore, it still faces the real bottlenecks: no registry of x402-enabled imagery services, no way to verify if an endpoint is legitimate or a honeypot, and no standard way to leave reviews other agents can query.

Deep Dives

Noah Levine (a16z) reframes the near-term TAM for x402: not the "autonomous machine economy," but payment rails for unbankable developers. Stablecoins are not replacing cards for existing merchants; they are enabling new ones — vibe coders, solo API builders, and entity-less microservices that processors cannot underwrite. These sellers are choosing stablecoins over nothing, not over cards. That makes Artemis's unique seller count, now around 2,500 cumulative across chains, the key metric for tracking supply-side expansion.

- Where Value Accrues in the Stack (and Where It Doesn't): The stack has 10 layers ordered by maturity. The critical insight from synthesizing Pantera, Petersen (Delphi), a16z, Multicoin, and LongHash: value accrues at constraint points, not plumbing.

| Layer | Description |

|---|---|

| Settlement chains | SOL, ETH/Base (or others) capture value on every transaction regardless of what sits above them. Non-disintermediable. Highest conviction layer. |

| Stablecoin issuers | Stablecoin issuers (Circle/USDC) benefit from liquidity network effects but face margin compression from the 56% Coinbase revenue share and future competition from bank-issued deposit tokens. |

| Facilitator layer | A value trap layer. Coinbase's facilitator 70% market share evaporated the instant they introduced a $0.001 fee in January 2026. Fifteen facilitators exist, all racing to zero. Dexter and PayAI are pivoting to adjacent layers (discovery via MCP integration, token narratives) because pure facilitation has no moat. |

| Discovery & Identity | Has the strongest winner-take-most dynamics but least mature. ERC-8004's singleton-per-chain design means one registry per network. Whoever reaches critical mass first becomes canonical. Machine identity market is projected at $21.4B in 2026, growing to $60.5B by 2035. Questions: Is this transaction volume or revenue? |

| Reputation | Least mature and potentially most valuable market. No standardized way exists to answer "should I trust this agent?" The projects attempting this (Recall, Theoriq, EAS) use different signal types — competition results, staking conviction, attestations — but none have built the full composite scoring system yet. |

- The TradFi Parallel Stack & Why It Doesn't Invalidate Crypto: Visa (Trusted Agent Protocol), Mastercard (Agent Pay), and Stripe (machine payments via x402) are all shipping production agentic commerce products. The market is splitting into two lanes: (i) Lane 1: Human-supervised agent commerce (McKinsey Levels 2–4). Agents shop for you, you approve, and payment settles on card rails. Visa TAP handles identity, Mastercard' s Agentic Tokens carry credentials, and Stripe abstracts the flow through PaymentIntents. This is the much larger near-term market. Cards work well here because users keep chargebacks, purchase protection, and rewards. No blockchain needed. (ii) Lane 2: Fully autonomous agent commerce (Level 5+). Agents transact directly with other agents, with no human identity to inherit, and often require sub-cent or programmable payments. Card rails do not work here: 2–3% fees make $0.001 transactions uneconomic.

Stripe is the bridge: x402 inside PaymentIntents via MPP gives merchants both lanes in one integration. Strongest proof x402 matters so far. Big threat to crypto-native facilitators, because merchants will pick Stripe over Dexter for settlement. Possible Hard Truth: Most near-term value in agentic commerce goes to Visa, Mastercard, and Stripe, not crypto-native players. Crypto wins later, when Lane 2 reaches real scale — and that depends more on AI progress than crypto. Timing matters: discovery is the blocker now, identity comes next, then reputation, then agent coordination. Invest in the layer about to break, not the one already built.

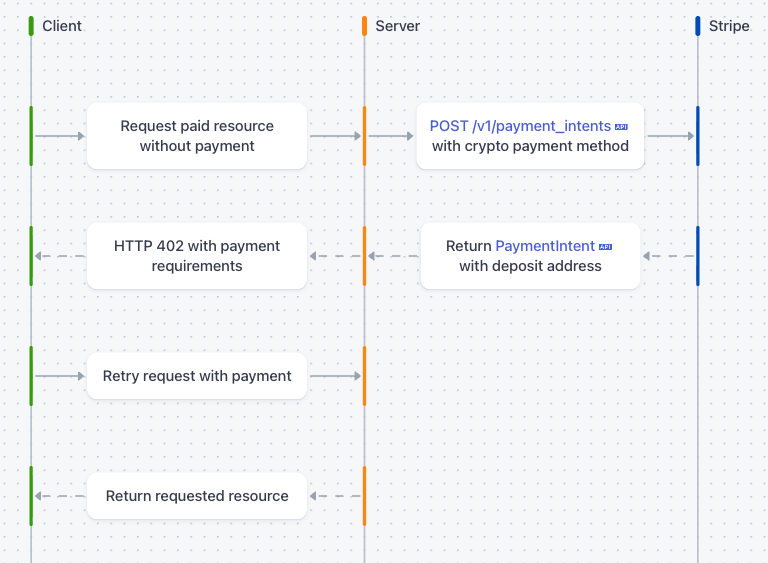

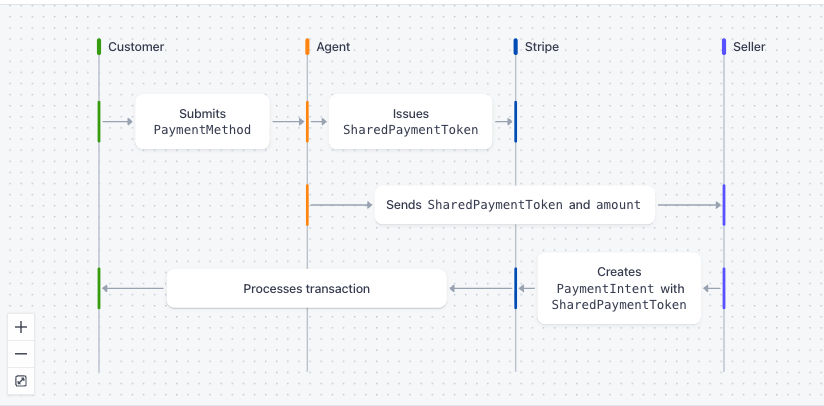

- How does Stripe support x402 & Fiat Payment through MPP? x402: Agents can request the product that they intend to pay for using Stripe's native payment_intents API which will return the deposit address which the agents will need to pay and transfer to.

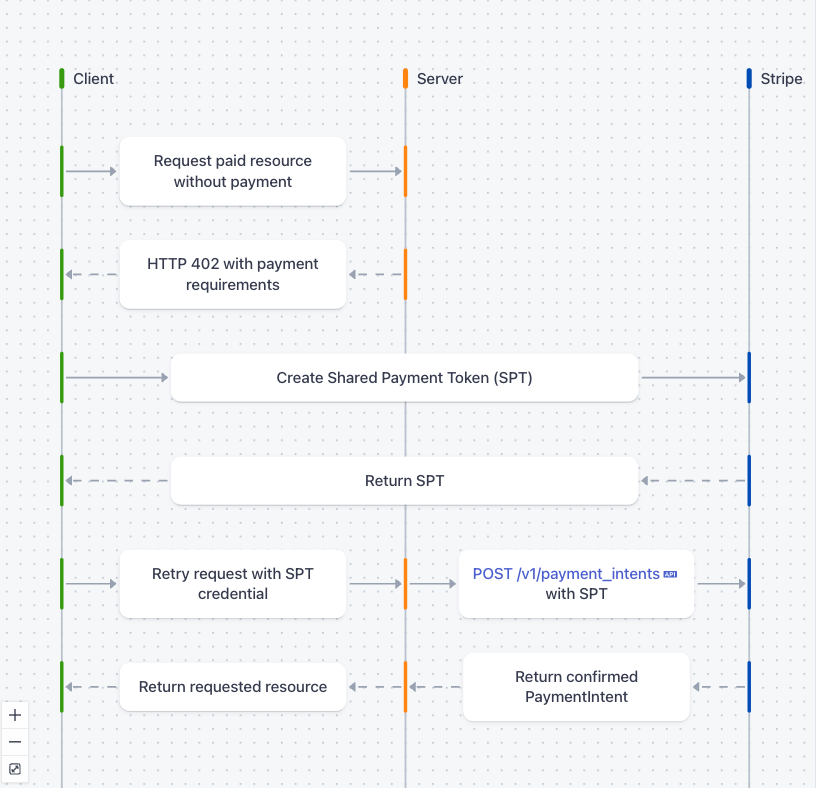

Traditional payment is supported using a Shared Payment Token (https://docs.stripe.com/agentic-commerce/concepts). A shared payment token defines how much an agent is allowed to spend and the expiry date. Using Agentic Commerce Platform (ACP), agents can create an agentic checkout session and complete payment seamlessly using API calls.

| Client (Buyer) | (i) Tries to access paid resources without payment, Server returns 402 Challenge. |

|---|---|

| Agent | (i) Requests for the shared payment token (SPT) and set the currency, max_amount and expires_at date. (ii) Agent calls the payment_intents API with SPT to make payment for a given service through the Agent Commerce Protocol (ACP) https://docs.stripe.com/agentic-commerce/protocol |

| Shared Payment Token (SPT) | (i) Scoped to a single seller merchant to ensure that other merchants are not able to use the SPT. |

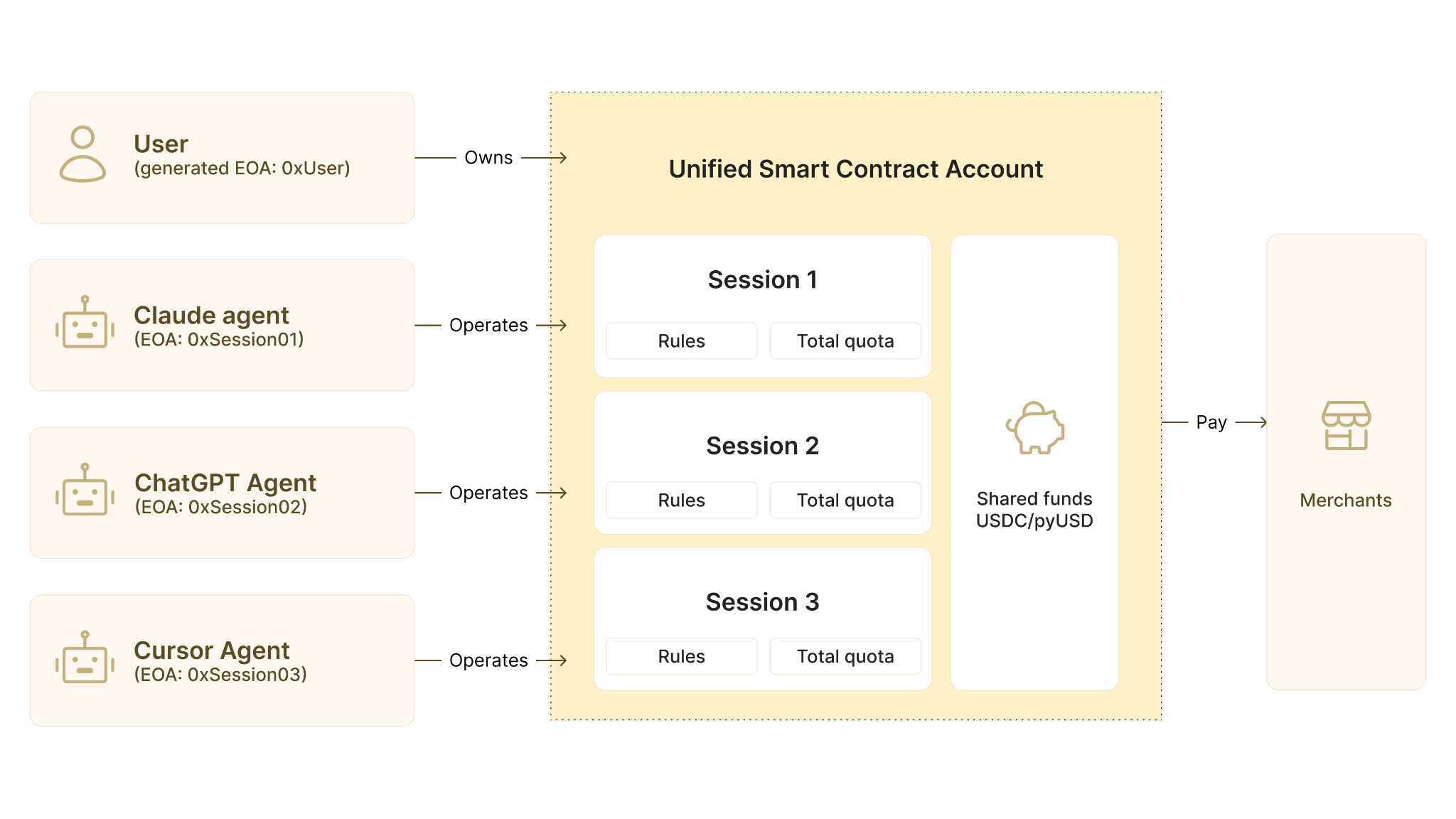

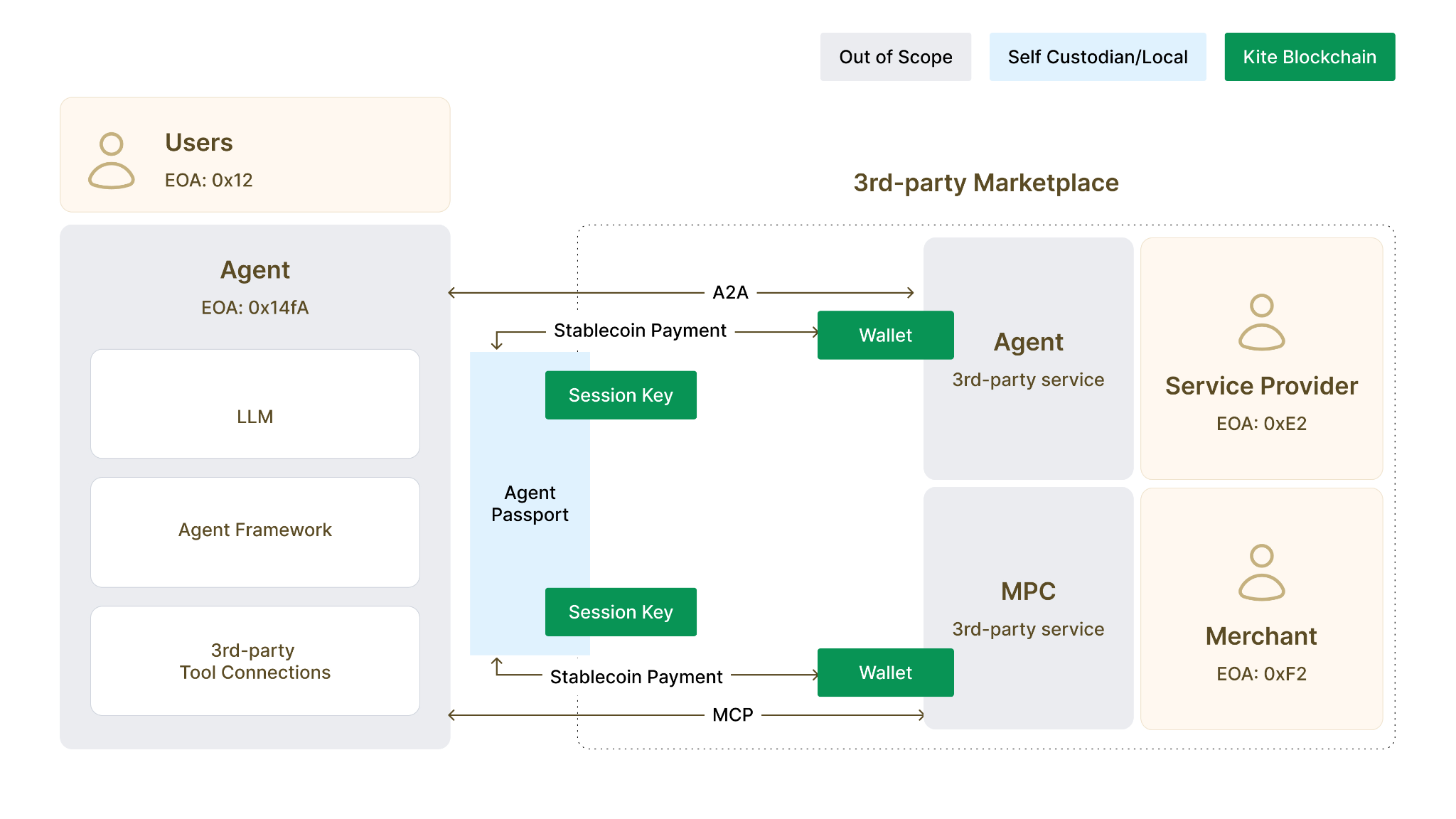

- Thoughts on how Agentic Commerce can advance: (i) Big company discovery: Stripe, Mastercard, Visa, and others could whitelist approved vendors, so agents can query a trusted discovery layer. Main question: will these companies govern it well enough to reduce fraud? (ii) Decentralized discovery: Open networks could let agents find verified services using reputation, compliance, and other trust signals. KiteAI is one example: https://docs.gokite.ai/get-started-why-kite/core-concepts-and-terminology. It is building identity and trust rails using cryptographic proofs and verifiable credentials. (iii) Skill-based discovery: Claude and OpenClaw use "skills" — folders and instructions loaded dynamically. One skill could list trusted infra vendors like Supabase and Vercel, plus commerce endpoints for each product. This is more modular and may be safer, because users import the skill files themselves. In effect, users whitelist providers directly instead of relying on a central registry. (iv) Discovery before payment: Autonomous payment is the goal, but discovery comes first. Near term, humans will likely still approve final payments. Even so, letting agents discover services and add products to buy would already be a big step forward. Today, trust is still too weak for fully autonomous payments.

People Profiles

(i) Cosmo Jiang (Pantera GP/PM): Ex-Nova River, Hitchwood, Apollo, Evercore. Focused on crypto x AI, especially AI agents, x402, and Digital Asset Treasuries. Argues autonomous agents are a long-term tailwind for blockchains. (ii) Sam Lehman (Pantera: Junior Partner): Joined in late 2025 to focus on crypto-AI. Ex-Symbolic Capital, Beacon. Studies the "agentified future," where AI agents use smart contracts and on-chain collateral for fast, capital-efficient transactions. (iii) Robbie Petersen (Delphi: Research Associate). Covers DeFi, stablecoins, and yield-bearing assets. Known for the "Fat Wallet Thesis" and for arguing revenue-sharing stablecoins could grow fast through app-layer distribution. (iv) Raghav Agarwal (LongHash: Principal): Focused on decentralized AI, data availability, and agentic commerce. Has written on missing discovery and reputation layers needed for autonomous agent transactions. (v) Noah Levine (a16z crypto Investment Partner) Joined in February 2026 after leading Visa's on-chain strategy. Focused on crypto, fintech, and payments. Known for cutting through AI agent payment hype and arguing real volume is far lower than reported. (vi) Lucas Shin (Artemis: Data researcher) Tracks crypto x AI with on-chain data. Built a wash-trading filter for x402, showing much of the volume was fake, but sees real demand in paywalls, API tools, and social distribution.

Authors of Summary:

Reference Paper

https://www.weforum.org/stories/2026/01/ai-agents-trust/