| The WhitePaper Reading Club Vietnam [01] - 25 September 2025 | |

|---|---|

| Berachain Honey Paper: Modern Problems, Modern Solutions | Alex (Research/Dev), Rongxin (WPRC), Ken (Berachain) |

Summary

An EVM-identical L1 blockchain that introduces Proof of Liquidity (PoL) - a novel consensus mechanism that aligns network security with application liquidity by rewarding validators based on their contribution to ecosystem liquidity rather than just stake size.

Why This Is Important

Changes L1 economics by directing block rewards to DApps and users rather than validators, solving the critical misalignment where chains spend billions securing millions in assets while applications struggle to bootstrap liquidity.

Key Innovation

POL is a dual-token model (BERA for gas/staking, BGT for governance/rewards) where validators must engage with DApps to earn rewards, creating a system where chain value derives from application success rather than vice versa.

Overview

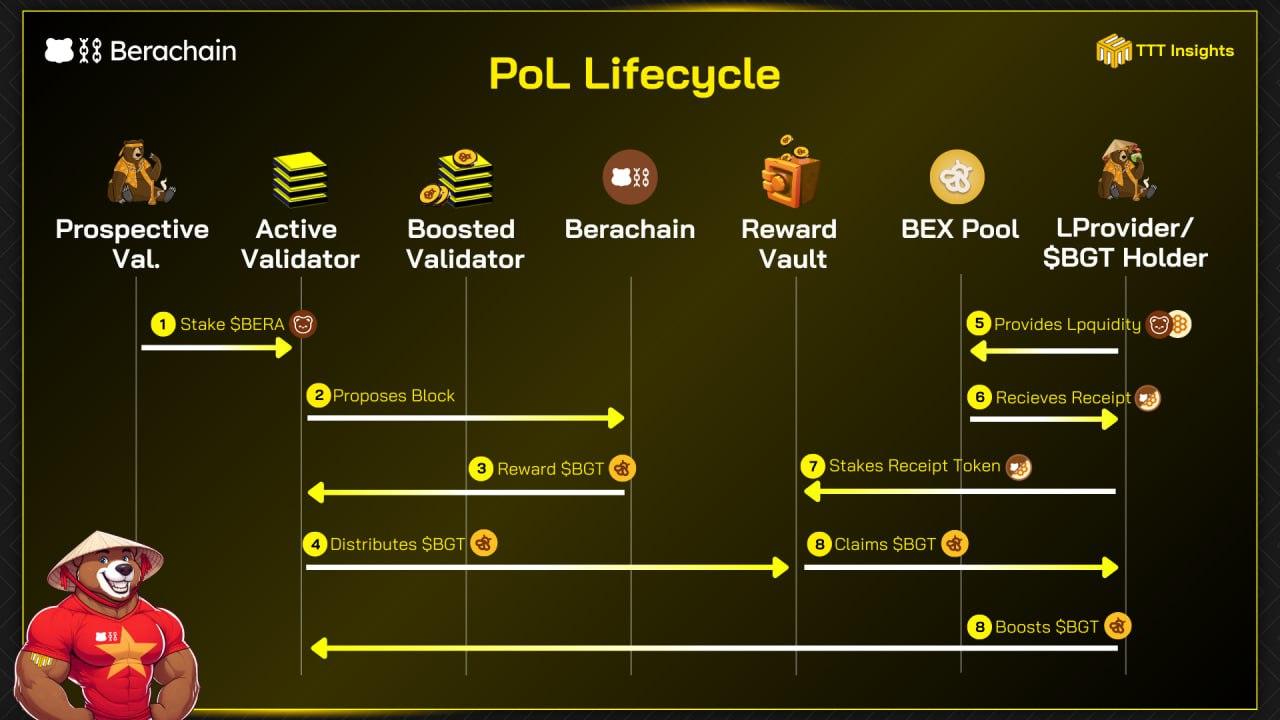

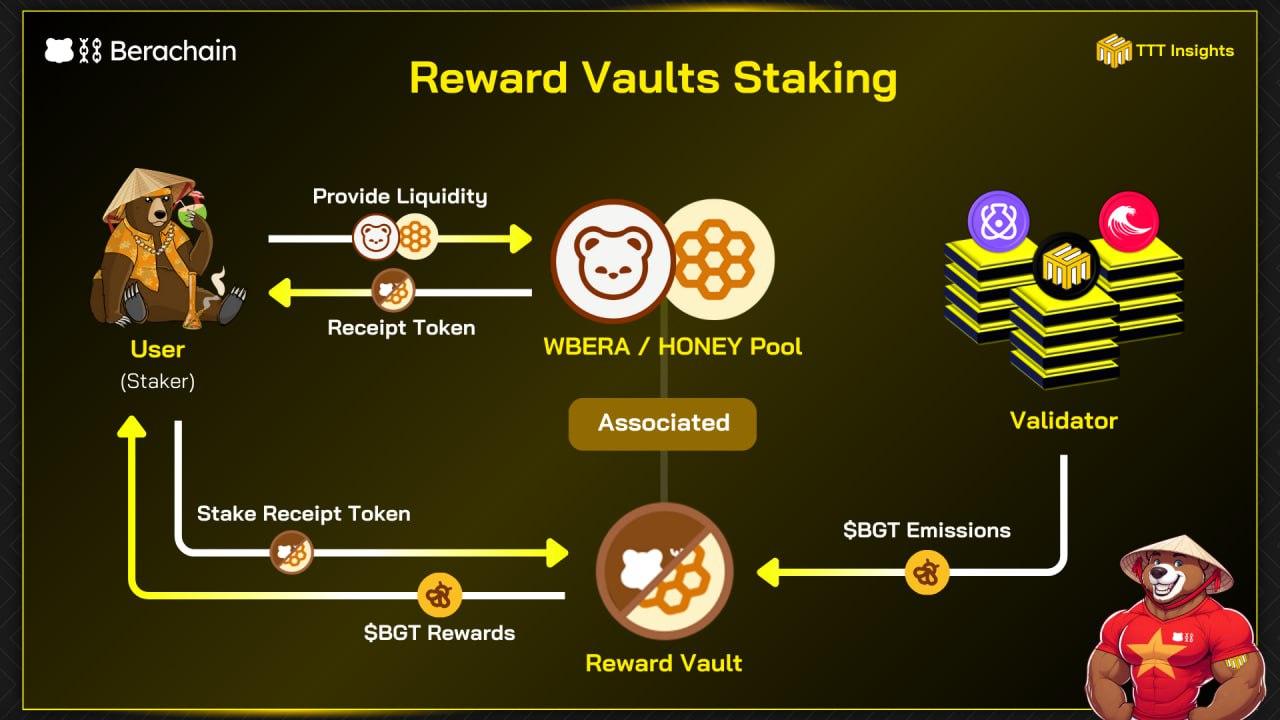

Berachain is an EVM-identical L1 that re-routes inflation toward real app usage via Proof of Liquidity (PoL). It splits roles between BERA (gas + staking) and BGT (non-transferable governance + rewards, burnable 1:1 into BERA). Validators join the active set by BERA stake (block chance ∝ stake), but the size of each block’s BGT reward depends on their BGT “boost” (delegations) under a concave curve that caps marginal gains to encourage decentralization. Most emissions must flow to app reward vaults (Curve-like gauges) where protocols bid for emissions with whitelisted tokens at posted exchange rates; validators route emissions, receive incentives, keep a commission, and share proceeds with their BGT boosters. Users earn BGT by staking PoL-eligible receipt tokens (e.g., LPs, RWA receipts, L2 bridge receipts) and can delegate or burn BGT to BERA, forming a self-correcting equilibrium. EIP-4788 proofs and BeaconKit wire consensus events to execution-layer rewards.

Background

From July 2024 Summary Key Points: (i) Tri-token: BERA (gas), BGT (governance), HONEY (stablecoin) NOW: just focused on 2 tokens (ii) Native protocols: Bex (DEX), Bend (lending), Berps (perps) to prevent monopolization. NOW: Removed (iii) Validators: Equal block production chance, BGT-proportional rewards (iv) "Gauges" terminology (Curve-inspired) (v) Concerns: OHM/3,3 parallels, Berafoundation trust, stablecoin dependency risks (vi) BeaconKit V2: Evolved from failed Polaris V1 monolithic architecture (https://docs.google.com/document/d/1yBD8TrK6o6kVGqJPGsdNp010KC4gk5X4hFgEvFUUzzk)

Team

Smokey (CEO), PapaBear (Lead Dev), Cami (Community), MVP, Yogi - Most of the team from Canada & USA. Bong Bears - The Origin of Berachain’s DeFi-Heavy Roots Reference Investors: Series A - Polychain Capital, Series B - Framework

Opinions

(What do you think) I like PoL’s direction: it turns chain inflation into a paid acquisition engine for apps instead of idle staking yield, and the BGT→BERA burn gives a clean self-correcting valve. The big swing factors will be (1) on-chain enforceability of incentive sharing—today’s “off-chain distribution” invites trust and coordination failures; wire at least a programmable floor split to boosters on-chain. (2) Concavity tuning (a,b,m)—too flat and whales capture emissions; too steep and small validators can’t boot; publish target ranges and auto-rebalance slowly per epoch. (3) Market quality—guard against wash trading / mercenary TVL by optimizing for “emissions per sustained liquidity/volume or verified action,” not raw deposits. (4) Governance bottlenecks—vault/token whitelists are powerful but can throttle composability; add fast-path, capped-size “probationary” listings with circuit breakers. (5) Gray-market boost rentals—non-transferable BGT reduces dump pressure but will spawn OTC delegation deals; better to provide a native, transparent delegation marketplace with escrow and slashing for bad actors. (6) Validator game theory—cap incentive commissions, require public, on-chain commission schedules, and surface a “realized APY to boosters” metric so boost flows to the fairest operators. If these execution details land, PoL can genuinely align users, apps, and validators; if not, it risks devolving to PoS with extra steps.

Components

(Key Innovations - focus on the innovations, and key parts)

| 1. Proof of Liquidity | (i) Change inflation to app demand. (ii) Validators win blocks by BERA stake, but most BGT emissions must be directed to app reward vaults (Curve-style). (iii) Apps post incentive rates (ERC-20 per BGT) to attract emissions; users stake PoL-eligible receipt tokens (LPs, RWAs, L2 bridge receipts) to earn BGT; validators route emissions to the best vaults, receive incentives, take a transparent commission, and share with their BGT boosters. (iv) Emission vs. boost is concave → diminishing returns, promoting decentralization and tying rewards to real usage. |

|---|---|

| 2. BGT/BERA Dynamics | (i) BERA = gas + staking (secures chain). BGT = non-transferable governance + reward token, burnable 1:1 → BERA (one-way). Earn BGT by (a) running/boosting validators (via BERA stake → validator; via vault staking → users). (ii)Delegate BGT to boost validators. (iii) Equilibrium: If app incentives > issuance → hold/boost BGT; liquidity deepens. If incentives < issuance → users burn BGT→BERA, shrinking claimants and lifting per-BGT yields until balance. |

| 5. Decentralization Features | (i)Active set by BERA stake with min/max stake caps per validator. (ii)Concave boost function + emission caps (via parameters a,b,m) limit whale advantage and keep inflation bounded. (iii)Validators compete on realized APY to boosters (commission/split/uptime/routing quality), encouraging stake/boost dispersion across operators. (iv)LST scale tempered by stake caps and diminishing returns; large pools must spin up more nodes with fresh boost. |

| 4. BeaconKit Infra | (i) Modular consensus framework delivering EVM identicality (unmodified execution clients) and fast finality/throughput. (ii) Uses EngineAPI and EIP-4788 so execution can verify consensus roots each block → PoL can mint/route BGT deterministically. (iii) Immediate execution & optimistic payload building reduce block times; client diversity without maintaining custom forks. |

| 6. Risk Mitigation | (i)“End of PoL” / rent-seeking: Market pressure for lower commissions; concave emissions penalize low-boost validators; publish on-chain commission schedules and enforce minimum booster splits. (ii)Centralization: reduce economies of scale; governance can adjust parameters slowly (epoch-based changes). (iii)Governance safety: Timelocks, delegates/guardians, and whitelist/circuit-breaker paths for vaults/tokens; probationary listings with kill-switches. (iv)Economic gaming: Minimum incentive rates; no lowering posted rate while residual tokens remain; monitor sustained liquidity/volume (not raw TVL) to curb wash liquidity. (v)Security coverage: Adjust issuance/params if BERA staked lags TVL; surface risk dashboards for MEV, validator behavior, and incentive concentration. |

Traction

Dune (need to remove outliers)

Questions/Answers (Thanks Berachain Team)

- Q: Should booster payouts be on-chain (programmable splits) to avoid trust/coordination issues? A: they basically are - validators are running a side car that handles distribution

- Q:How to prevent wash liquidity—what metrics (TVL, volume, fees, retention) should gate emissions/eligibility? A:this is up to governance, they're going to submit an RFP to track data to ensure that vaults are being used appropriately.

- Q:How to cap LST/boost cartels (stake caps, emission ceilings, concavity) and add timelocks/ratchets to stop capture? A:exactly what you said, stake caps and concavity are the biggest too. There aren't really any big cartels right now.

- Q: How does the concave emissions function (a, b, m) change validator incentives—and what ranges balance decentralization vs. small validator viability? A:ensures that new validators without boost will get boost so long as they are allocating effectively as the marginal returns of boosting to a large existing boosted validator is lower returns than one without boost

References

[1] Dinesh Kumar, Duraimutharasan, Shanthi, Vennila, Prabu Shankar and Senthil. Comparative Analysis of Transaction Speed and Throughput in Blockchain and Hashgraph: A Performance Study for Distributed Ledger Technologies. Journal of Machine and Computing, 3(4), 2023. https://pdfs.semanticscholar.org/2e97/1b66175ee27ed558fdcfafb3c645ddd3d68d.pdf

[2] https://blog.berachain.com/blog/the-pol-post

[3] https://blog.berachain.com/blog/the-fat-bera-thesis

[4] Urban J. Jermann. A Macro Finance Model for Proof-of-Stake Ethereum. National Bureau of Economic Research (NBER), 2023. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4335835

[5] https://docs.curve.fi/assets/pdf/CurveDAO.pdf

[6] Vitalik Buterin. Possible futures of the Ethereum protocol, part 3: The Scourge. 2024. https://vitalik.eth.limo/general/2024/10/20/futures3.html

[7] Li Li. Mitigating Challenges in Ethereum's Proof-of-Stake Consensus: Evaluating the Impact of EigenLayer and Lido. 2024 https://arxiv.org/abs/2410.23422

[8] https://research.lido.fi/t/is-lido-good-for-ethereum/5520

[9] https://notes.ethereum.org/@djrtwo/risks-of-lsd https://www.mdpi.com/1099-4300/25/9/1320

[10] Alex Stokes, Ansgar Dietrichs, Danny Ryan, Martin Holst Swende, light-client. EIP-4788: Beacon block root in the EVM. 2022 https://eips.ethereum.org/EIPS/eip-4788

[11] https://github.com/ethereum/execution-apis/blob/main/src/engine/common.md

[12] https://docs.cometbft.com/v0.37/spec/abci/

[13] https://ethresear.ch/t/considering-client-diversity-through-the-lens-of-network-performance/18885