| The WhitePaper Reading Club Singapore - 16th August 2025 | |

|---|---|

| Circles 2.0: Reimagining Money for a Multipolar World | Song Lin, Cheng Ye |

Summary

Circles 2.0 is a decentralized money system where everyone generates their own personal currency (CRC), and trust makes it usable everywhere.

Why This Is Important

It gives everyone equal access to money, keeps it fair, and stops a few people or governments from controlling it.

Key Innovation

Circles lets people generate their own money (CRC) that is backed by trust, not banks. The trust network controls who can use and accept each currency, making the system fair and resistant to fake accounts.

Overview

(i) Everyone makes a little CRC every hour. (ii) You can spend CRC with people you trust. (iii) Old money loses a bit of value each year to keep the system balanced. (iv) Prices stay steady because new money and shrinking old money balance out.

Background

(i) Distributed issuance: Everyone mints the same flow of new currency, no one controls it all. (ii) Trust=Acceptance: Users accept each other’s currencies through trust links; Through friends-of-friends, we can make transactions outside of our direct network. (iii) Demurrage: Money slowly loses value over time, so money keeps moving instead of piling up; (iv) People can pool their tokens into a group currency, making it easy to trade and organize together.

Team

(i) Martin Köppelmann: Co-founder of Gnosis, leading the development of Circles 2.0. Started talking about this since 2015. (ii) Paul Boes: Developer who contributed to the technical aspects of Circles 2.0, and co-author of paper. Previously PhD in Philosophy of Physics at Oxford (iii) Gnosis Team: The team behind the Gnosis Chain, providing the infrastructure for Circles 2.0.

Components

(Key Innovations - focus on the innovations, and key parts)

| Problem Statements | Problems with current fiat systems: (i) Centralization – Money issuance controlled by a few, enabling exploitation and undue influence. (ii) Unequal access to new money – Loans favor those with better credit (Cantillon Effect). (iii) Lack of transparency – Monetary policies are complex, leading to poor decisions (e.g., 2008 crisis, Zimbabwe hyperinflation). (iv) Global inequality – Reserve currencies (like USD) allow some governments to shift inflation impacts onto others.Problems with current cryptocurrencies: (i) Wealth concentration – Most coins are held by a small percentage of the population, leaving the majority with little influence. (ii) Fixed supply limitations – Cannot adjust supply to maintain stable value, reducing usefulness as a practical medium of exchange. | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Circles protocol rules/ concepts | 1. Universal access: Anyone can create an account without any gatekeeping. No know your customer (KYC) checks.2. Distributed issuance: Each account has the right to create their own, individual CRC at a rate of 1 CRC per hour.3. Demurrage: Every CRC gradually loses nominal value at a rate of 7% per year (like taxes).4. Rule of Trust: Accounts can trust one another. If account A trusts account B, then anyone in the network holding CRC created by B can swap them, at any time, for any CRC held by A, at a rate 1:1. 5. Groups: Anyone can create a group and add accounts as its members, by trusting them. Groups support their own CRC, however these CRC are not issued continuously, instead they can be created from and redeemed against CRC that have been created by its members, at a rate 1:1. | |||||||||

| Macro economics | Fairness to Wealth InequalityRemember there are two forces acting as inflow and outflow on money supply:1 CRC per Day Issuance (Growth)7% Demurrage (Decay)- Every person continuously issues 1 CRC into the system.- This guarantees newcomers start with the same “flow” of new tokens as early adopters.- Macro effect: The money supply keeps expanding in a distributed and egalitarian way. No- Every year, balances shrink by ~7%.- This prevents old, inactive accounts from hoarding and ensures that money keeps circulating.- Macro effect: Wealth concentration gets reduced over time; the gap between rich and poor narrows.The results: (i) Both accounts earn the same 8,479 CRC from issuance. (ii) Larger balances shrink more due to proportional demurrage. (iii) Over time, balances tend to converge toward the ~120k CRC equilibrium.Price stability: (i) In Circles, each person’s balance converges to about 120k CRC. (ii) This means the total money supply automatically grows or shrinks in proportion to the population. When the population increases, more CRC is issued; when it decreases, issuance falls. As a result, the money supply stays aligned with the number of people using it. (iii) In the long run, this balance keeps the price of goods steady instead of spiraling up (inflation) or down (deflation). (iv) Read more: Overlapping-Generations ModelFair access to Money Supply: New-joiners can build a share of the money supply quickly, regardless of the distribution when they joined. (no disadvantage to people joining later). All users benefit equally from the issuance of money. Fairness to Issuance: (i) In today’s world, governments and banks decide who gets new money and profit from creating it (this profit is called seigniorage). (ii) Circles spreads this power out: everyone creates their own money, so the profit from new money is shared equally among all users. | 1 CRC per Day Issuance (Growth) | 7% Demurrage (Decay) | - Every person continuously issues 1 CRC into the system.- This guarantees newcomers start with the same “flow” of new tokens as early adopters.- Macro effect: The money supply keeps expanding in a distributed and egalitarian way. No | - Every year, balances shrink by ~7%.- This prevents old, inactive accounts from hoarding and ensures that money keeps circulating.- Macro effect: Wealth concentration gets reduced over time; the gap between rich and poor narrows. |

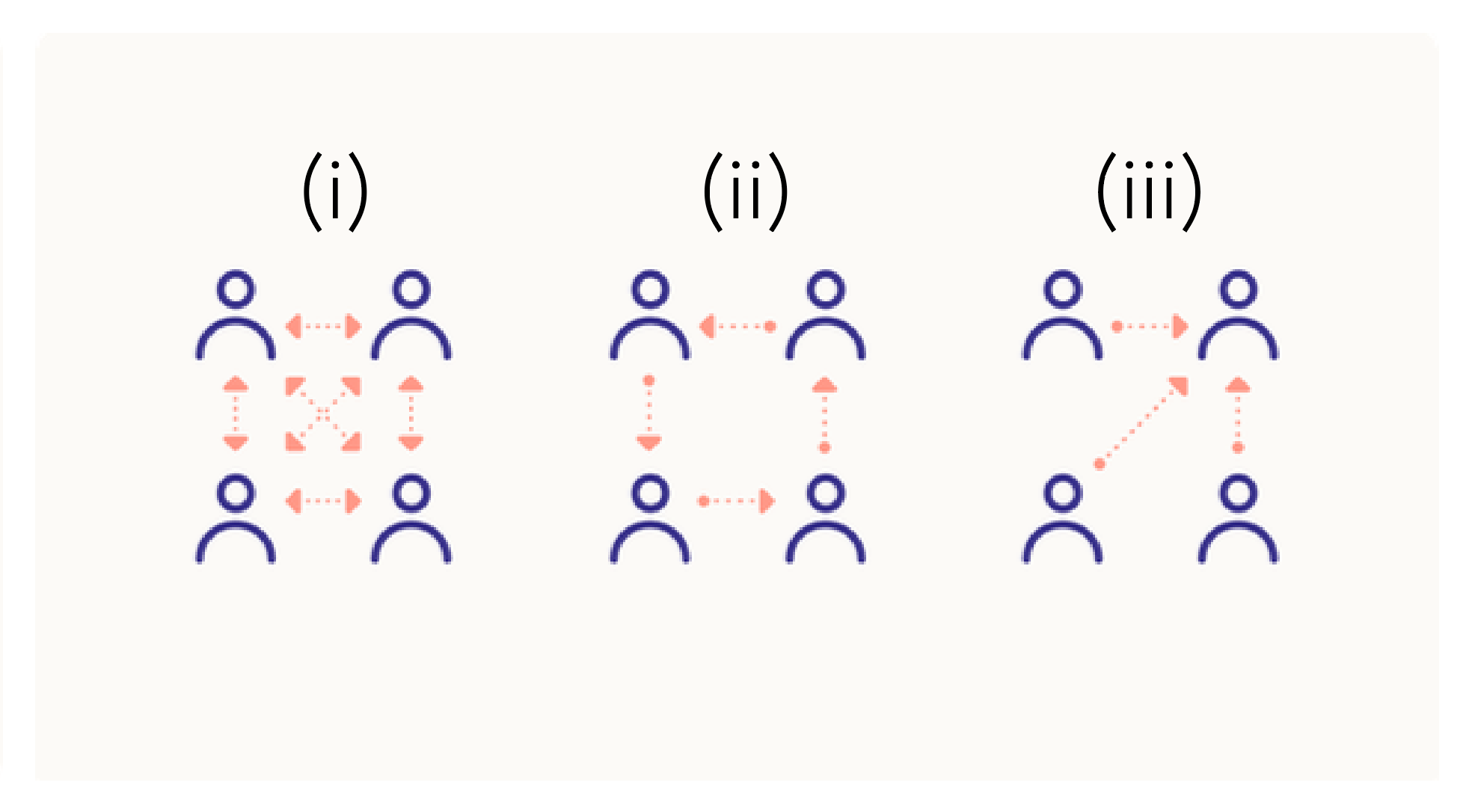

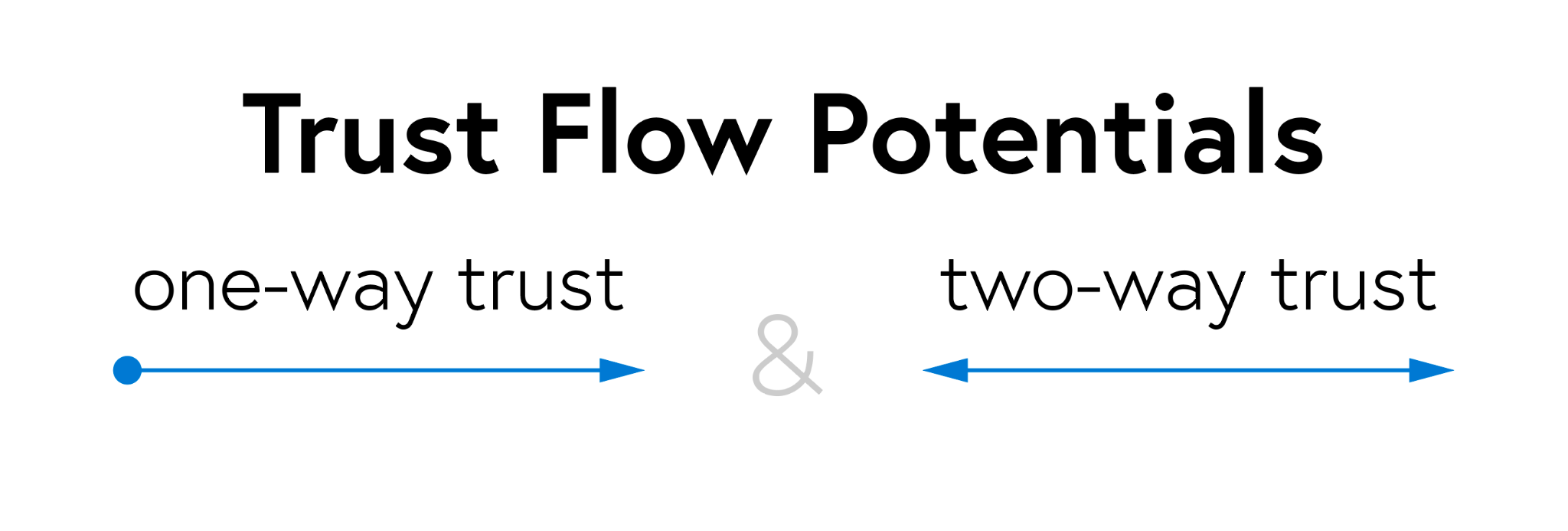

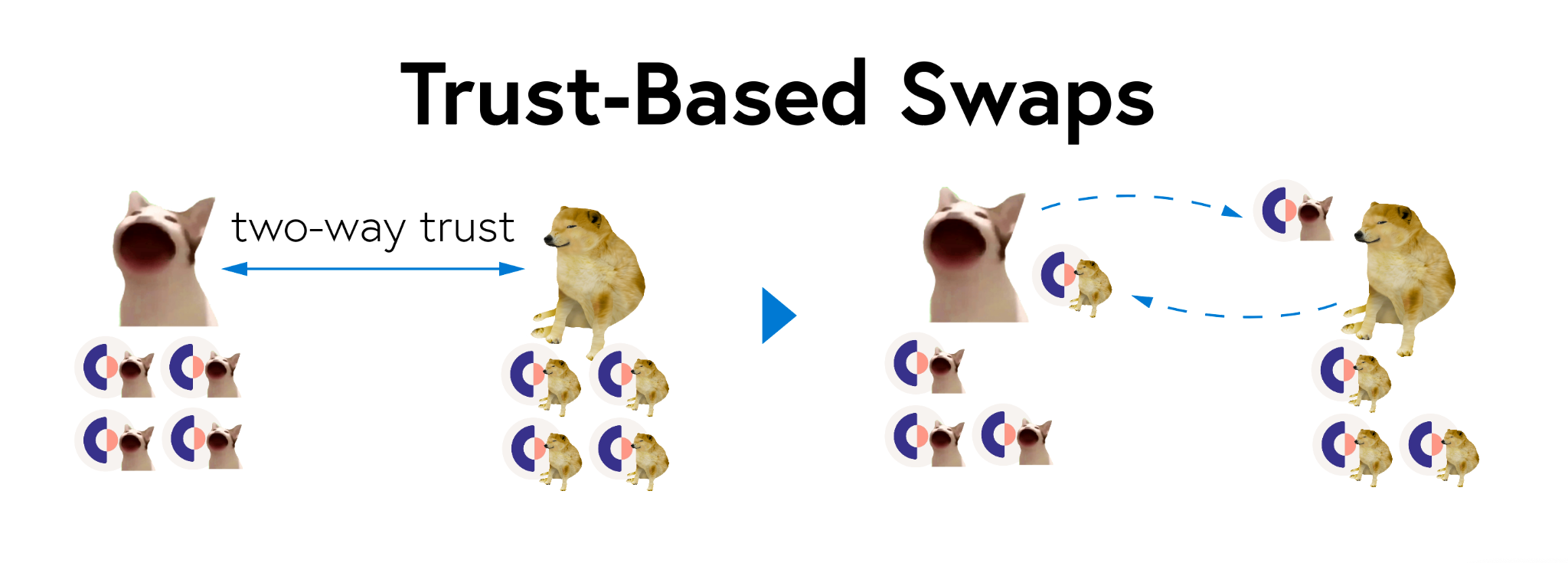

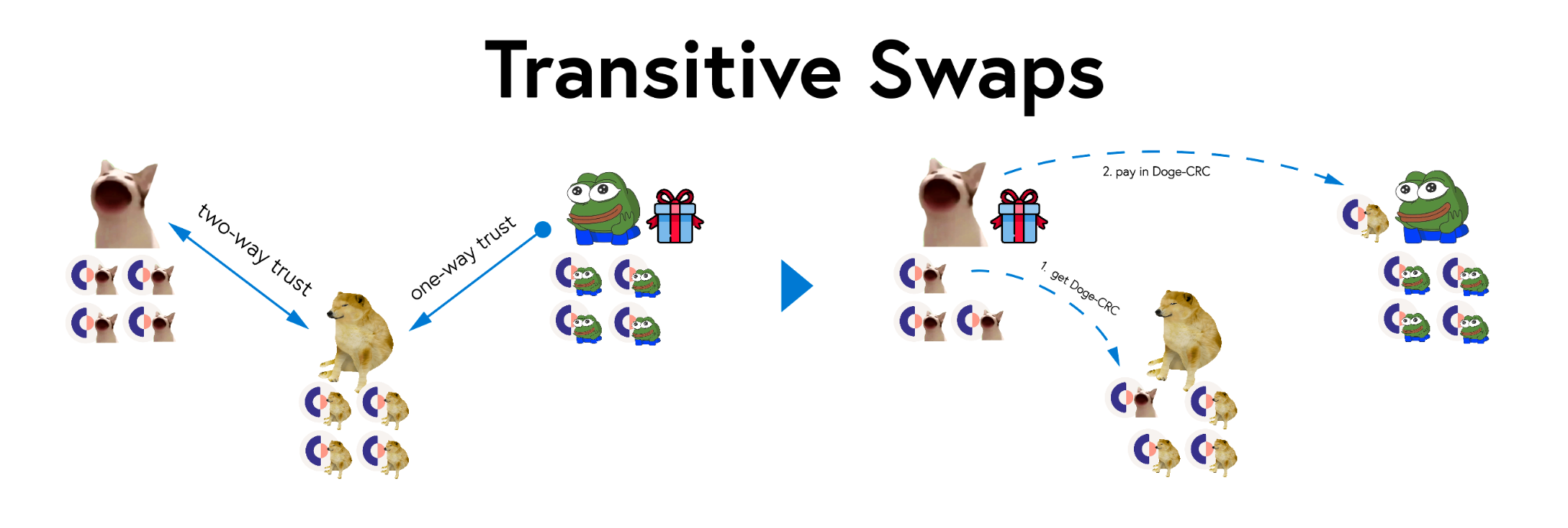

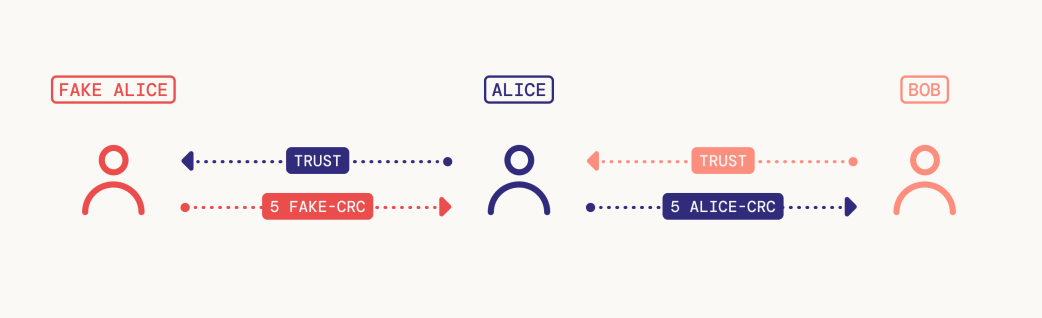

| 1 CRC per Day Issuance (Growth) | 7% Demurrage (Decay) | | | | | | | | | | | - Every person continuously issues 1 CRC into the system.- This guarantees newcomers start with the same “flow” of new tokens as early adopters.- Macro effect: The money supply keeps expanding in a distributed and egalitarian way. No | - Every year, balances shrink by ~7%.- This prevents old, inactive accounts from hoarding and ensures that money keeps circulating.- Macro effect: Wealth concentration gets reduced over time; the gap between rich and poor narrows. | | | | | | | | | | | Micro economics | CRCs are non-fungible: (i) Fungible money: Like $10 — everyone’s $10 is exactly the same and interchangeable. (ii) Non-fungible in Circles: Each account creates its own personal CRC.Alice creates Alice-CRC, Bob creates Bob-CRC, etc.Your wallet can hold a mix of different CRCs.Example: Alice sees 10 CRC in her wallet, but it could be: 3 Alice-CRC, 5 Bob-CRC, 2 Charlie-CRCTrust graphs with global fungibility (a route always exist for any transfers):(i) Everyone trusts everyone else (ii) Ring graph (iii) Star graph (*person everyone trusts needs to have enough liquidity)Trust-based swaps (e.g. Two-way trust: Popcat-CRC is fungible with Doge-CRC):Transitive Transfers (I.e Trade through a trust connection):Trust chain: (i) Popcat and Doge trusts each other. (ii) Pepe trusts Doge (but doge does not trust Pepe)Step 1 – Indirect acceptance: Because of the trust chain, Pepe can accept CRC from anyone Doge trusts, even if he doesn’t know them directly. Popcat now wants to buy a giftbox from Pepe (who he does not trust).Step 2 – Swap happens: (i) Popcat swaps his Popcat-CRC for Doge-CRC with Doge. (ii) Now Popcat can use Doge-CRC to pay Pepe. The system automatically swaps it through the trust chain: Popcat→ Doge → PepeStep 3 – Pepe ends up holding 1 Doge-CRC (transitively swapped), even though he never interacted with Doge directly.Conclusions: (i) Trust affects your net worth: Who you trust directly impacts the currencies you can accept and your overall purchasing power. (ii) Intermediaries need enough money: People in the middle of the chain (e.g. Doge) must have enough CRC to complete the swaps; otherwise, the transaction can’t fully go through.Resistance against malicious partiesSybil attack: Creating fake accounts to mint extra CRC (e.g., 100 accounts → 100 CRC/hour).Trust rule limits this: Economic influence depends on who others actually trust.Example: (i) Alice creates a second account, FakeAlice, and can mint 2 CRC/hour in total. (ii) Bob only trusts Alice’s main account, so he is only exposed to 1 CRC/hour. (iii) FakeAlice’s CRC is useless to Bob; it stays with Alice.Result: (i) Alice’s effective issuance rate is still 1 CRC/hour through Bob. (ii) Alice will be the one getting Fake-Alice CRC, while Bob still gets Alice-CRC | | | | | | | | | | | [Groups] | Organizations vs Groups: (i) Organizations can send/receive CRC but don’t create money. (ii) Groups create their own currency (Group-CRC) using members’ CRC as collateral.How Group-CRC works: (i) Members swap personal CRC 1:1 for Group-CRC stored in the Group vault. (ii) Group-CRC can be redeemed 1:1 anytime, keeping total CRC supply balanced.Groups for shared interests: (i) People organize around location, interests, communities, events, education, or enterprises. (ii) Multiple Groups can exist for the same type of users independently.Transitive trust and federations: (i) Groups can trust humans or other Groups. (ii) Membership can be transitive, letting sub-Groups or federations issue Group-CRC.Active vs Passive Groups: (i) Passive: membership given automatically (e.g., location-based). (ii) Active: users must apply or meet rules (e.g., DAOs, cooperatives). (iii) Groups can use custom rules: limit supply, require collateral, lock redemption, or enforce membership criteria. | | | | | | | | | | | Other Considerations | Why 7% demurrage? (i) Empirically, long term average increase in US Dollar supply is slightly below 7% (ii) The Dragon Chamberoretically, stable 120,804 is reached after 80 years, a person’s lifespan. Matches lifetime creation vs. decay. Someone joining today shouldn’t be disadvantaged by competing with 80-year-old accounts that have accumulated decades of unused CRC. Decay ensures older coins fade out, letting new issuances stay relevant.Loans: (i) In Circles, banks cannot create new money—they can only lend CRC that people have deposited. (ii) Banks act as middlemen, charging fees to check if someone is trustworthy enough to borrow. (iii) Because they can’t make extra money from creating loans, banks compete for deposits and may offer higher interest to attract people. (iv) This shifts part of the old “bank profit” to depositors, while banks still earn money for their services. (v) Example: Alice borrows 10,000 CRC from Bob, makes 11,000 CRC in a year, repays Bob, and keeps 1,000 CRC profit. Bob earns 7% interest (because if not loaned out, it would have depreciated by 7%), which protects him from his CRC losing value over time.Should AI agents have their own account? (i) CRC is a currency that should only be created by people. As such, AI agents and applications are encouraged to exist on Circles, however they should be using the Organization accounts that we discuss below and that cannot create CRC. | | | | | | | | | | | Comparisons | VS Circles 1.0Concepts are mostly the same except:FeatureCircles 1.0Circles 2.0Issuance & Demurrage1 CRC/minute (525,600 per year), built-in inflation mechanism.Fixed 1 CRC/hour (8,760 per year), built-in 7% burn on-chain.Group / Organization SupportVery briefly mentionedNative group currencies with collateralized mintingVS Universal Basic Income (UBI): (i) Circles was once seen as a form of UBI. (ii) UBI is a top down approach to provide income security. A central authority pays a basic income to everyone. (iii) A typical UBI gives you a big chunk of money—around 25–30% of what you normally earn—so you can actually spend it on stuff you need. (iv) Circles give each person new money too, but it’s much smaller, around 9% of what you might expect from a UBI. (v) So, while it’s something extra, it doesn’t replace your income—it just adds a little boost to your spending. | Feature | Circles 1.0 | Circles 2.0 | Issuance & Demurrage | 1 CRC/minute (525,600 per year), built-in inflation mechanism. | Fixed 1 CRC/hour (8,760 per year), built-in 7% burn on-chain. | Group / Organization Support | Very briefly mentioned | Native group currencies with collateralized minting | | Feature | Circles 1.0 | Circles 2.0 | | | | | | | | | | Issuance & Demurrage | 1 CRC/minute (525,600 per year), built-in inflation mechanism. | Fixed 1 CRC/hour (8,760 per year), built-in 7% burn on-chain. | | | | | | | | |

| Group / Organization Support | Very briefly mentioned | Native group currencies with collateralized minting | | | | | | | | | | Takeaways | (i) Everyone becomes a central bank (ii) No government needed (iii) Built-in wealth redistribution (iv) Social networks become financial networks (v) Global but local | | | | | | | | | |

Questions

(i) What is the difference between Circles 1.0 and Circles 2.0?

(ii) How are trust paths determined in Circles? If there are multiple ways to reach someone, does the system always drain tokens from the most trusted person, follow the shortest path, balance across paths, or prefer super-connectors?

(iii) Who is maintaining this network? They earn based on CRC fees when people mint?

(iv) How would organisation accounts function in real life?

(v) Just like it’s common for people to hold multiple bank accounts (e.g., one for work expenses and one for personal use), someone might want two Circles accounts for genuine reasons. But at the same time, another person might do this just to farm extra tokens. How do we distinguish?

(vi) Does the burning event happen at the same time for everyone? Wondering if anyone could dodge the demurrage by temporarily transferring money out of account.

(vii) Is the group-CRC also non-fungible in the sense that it keeps metadata on what to unwrap to?

(ix) How does Circle tie into DIDs and SocialFi? What about privacy or is there doxxing concern?

(x) Possible to issue CDC vouchers that are backed by this protocol? Is it possible to collect GST by relying on CRC mechanisms?

(xii) Is our current infrastructure able to support such a protocol at scale? What would be the technological specifications?

(xiii) Which country/ community would likely be the first to adopt? Which country/ community would likely resist this the most?

(xiv) Would inheritance mechanisms be effectively eliminated with Circles?